Strategy Essentials

Construction: Sell 1 In-the-Money (ITM) Call + Buy 2 Out-of-the-Money (OTM) Calls, same expiration

Maximum Profit: Unlimited

Maximum Loss: Limited (occurs if stock ends near the long call strike)

Breakeven Points: Two – lower breakeven at short call strike, upper breakeven above the long calls

Best Market Context: Anticipated sharp upside move with low implied volatility entry

Complexity Level: Intermediate to advanced (requires ratio spreads understanding

Introduction

The call backspread, also called the reverse call ratio spread, is a bullish options trading strategy designed for traders who expect a sharp upside breakout in the underlying asset. Unlike a single long call, which gives unlimited upside but requires a significant upfront premium, the call backspread uses a ratio of short and long calls to reduce entry cost while still keeping unlimited profit potential.

In its most common form, the strategy is built as a 2:1 ratio:

- Sell one in-the-money (ITM) call at a lower strike.

- Buy two out-of-the-money (OTM) calls at a higher strike, same expiration.

This creates an asymmetric profile:

- Unlimited profit if the underlying rallies hard.

- Limited risk if the stock stalls or moves moderately.

- Often, the position can even be opened at low or zero cost, making it attractive in situations where a trader expects an explosive move.

Construction of a Call Backspread

Basic Setup

- Sell 1 ITM call (lower strike).

- Buy 2 OTM calls (higher strike).

- All contracts must be on the same underlying, same expiration.

The ratio spread design ensures:

- The short ITM call generates premium income to help finance the two long calls.

- The long OTM calls provide leveraged upside exposure.

Example of Construction

Assume stock X trades at $90 in April.

- Sell 1 April 85 call at $700.

- Buy 2 April 95 calls at $350 each = $700.

➡️ Net entry cost = $0 (trade placed for no debit/credit).

This balance may not always exist perfectly, but it demonstrates the concept. In real markets, a trader may enter for a small debit or small credit.

Unlimited Profit Potential

One of the biggest attractions of the call backspread is its open-ended upside. Once the underlying trades above the long call strikes, the long calls begin to dominate.

Profit Formula

- Maximum Profit: Unlimited.

- Profit occurs when underlying ≥ (2 × long strike − short strike ± net premium).

- At expiration, profit = intrinsic value of long calls − intrinsic value of short call ± net premium.

Profit Scenarios

Continuing with X stock example (short 85 call, long two 95 calls):

- At $95:

- Short 85 call = $1,000 loss.

- Long 95 calls expire worthless.

- Net = −$1,000 (max loss point).

- At $100:

- Short 85 call = $1,500 loss.

- Long 95 calls = $1,000 total gain.

- Net = −$500 loss.

- At $105:

- Short 85 call = $2,000 loss.

- Long 95 calls = $2,000 total gain.

- Net = breakeven.

- At $120:

- Short 85 call = $3,500 loss.

- Long 95 calls = $5,000 total gain.

- Net = $1,500 profit.

- At $140:

- Short 85 call = $5,500 loss.

- Long 95 calls = $9,000 gain.

- Net = $3,500 profit.

➡️ Beyond the upper breakeven, profits rise linearly with stock price.

Limited Risk

The strategy’s maximum loss is capped and occurs when the underlying finishes exactly at the long strike.

- At that point:

- Short call is deep ITM, causing losses.

- Both long calls expire worthless.

- Result = defined, limited loss.

Max Loss Formula

Max Loss = (Long Strike − Short Strike) − Net Credit (or + Net Debit)

Example

If X stock ends at $95 at expiration (long strike):

- Short 85 call = $1,000 intrinsic loss.

- Long 95 calls expire worthless.

- Net = −$1,000 = max loss.

This loss amount does not increase further regardless of how close the stock finishes near $95.

Breakeven Points

The call backspread has two breakeven levels:

- Lower Breakeven: Short call strike (85 in the X example).

- Below this, all options expire worthless → no loss if trade was opened for zero cost.

- If entered for debit, small debit = loss.

- If entered for credit, small credit = profit.

- Upper Breakeven: Long strike + maximum loss.

- Formula = Long Strike + (Long Strike − Short Strike − Net Credit).

- In the DEF example: 95 + (95−85) = 105.

➡️ From $105 upwards, unlimited profit potential begins.

Detailed Example

Let’s build a full payoff table with different outcomes.

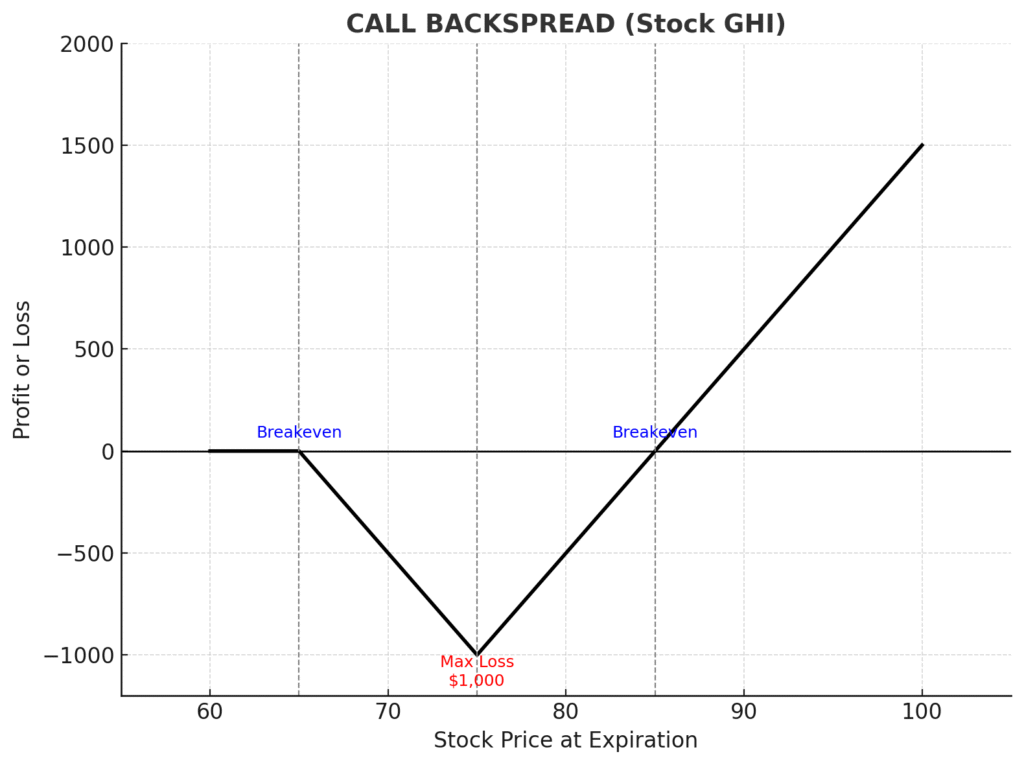

Stock GHI trading at $70.

- Sell 1 June 65 call at $700.

- Buy 2 June 75 calls at $350 each ($700).

- Net = $0.

| Stock Price at Expiration | Short 65 Call | Long 75 Calls (x2) | Net Result |

|---|---|---|---|

| $60 | $0 | $0 | $0 |

| $65 | $0 | $0 | $0 |

| $70 | −$500 | $0 | −$500 |

| $75 | −$1,000 | $0 | −$1,000 (max loss) |

| $80 | −$1,500 | $1,000 | −$500 |

| $85 | −$2,000 | $2,000 | $0 (breakeven) |

| $90 | −$2,500 | $3,000 | +$500 |

| $100 | −$3,500 | $5,000 | +$1,500 |

➡️ Clear pattern:

- Max loss at $75 = $1,000.

- Breakeven at $65 and $85.

- Unlimited gains beyond $85.

When to Use a Call Backspread

- Earnings announcements: when a trader expects a huge move.

- Volatility plays: ideal when implied volatility is low, giving cheaper call premiums.

- Breakout trades: strong technical setups where stock may surge.

This strategy is less effective in sideways or slow-moving markets.

Greeks Analysis

- Delta: Initially negative (due to short ITM call), but flips strongly positive if stock rallies above long strikes.

- Gamma: High positive gamma – position responds aggressively to sharp moves.

- Vega: Positive vega – benefits from rising implied volatility.

- Theta: Negative – time decay hurts unless a big move happens.

Advantages

- Unlimited profit potential.

- Limited, well-defined risk.

- Often entered for low or no cost.

- Good hedge for sudden market rallies.

Disadvantages

- Requires strong, timely move.

- Max loss occurs if stock finishes near long strike.

- Complex compared to simple long calls.

Variations

- 3:2 ratio backspread (sell 2, buy 3).

- Credit vs debit entry: some backspreads can be entered for net credit.

- Applicable on stocks, ETFs, indexes, futures options.

Comparison with Other Strategies

- Long Call: simpler, but more expensive.

- Bull Call Spread: limited profit, cheaper but capped upside.

- Call Ratio Spread: different payoff (not unlimited).

The call backspread offers the best convexity for explosive upside.

FAQ

1. What is a Call Backspread strategy?

A call backspread, or reverse call ratio spread, is an options strategy where a trader sells one in-the-money call and buys two out-of-the-money calls with the same expiration. It is a bullish strategy with unlimited profit potential and limited downside risk.

Q2. Is the Call Backspread bullish or bearish?

It is a bullish strategy. The payoff becomes highly profitable if the underlying stock makes a strong upward move beyond the breakeven level.

Q3. What is the maximum profit of a Call Backspread?

The maximum profit is unlimited, as the long calls continue to gain value as the underlying stock rises.

Q4. What is the maximum loss of a Call Backspread?

The maximum loss is limited and occurs when the stock finishes exactly at the long call strike. At that point, the long calls expire worthless and the short call is in-the-money.

Q5. How do you calculate the breakeven points?

- Lower breakeven = short call strike (if entered at zero cost).

- Upper breakeven = long call strike + (long strike − short strike ± net debit/credit).

Q6. Why is the Call Backspread sometimes called a “reverse call ratio spread”?

Because it reverses the classic ratio spread. Instead of selling more calls than buying, you buy more calls than you sell, giving unlimited upside potential.

Q7. When should you use a Call Backspread?

Best when you expect a sharp rally, often before events like earnings, major news, or technical breakouts.

Q8. Is the strategy sensitive to volatility?

Yes. It has positive Vega, meaning it benefits from an increase in implied volatility after the trade is placed.

Q9. What happens if the stock price falls below the short strike?

All options expire worthless, and if the trade was initiated for zero cost, the net result is no loss and no gain.

Q10. How does time decay (Theta) affect a Call Backspread?

The position typically has negative Theta, so time decay works against it unless a strong upward move happens.

Q11. Is the Call Backspread margin-intensive?

It requires margin because of the short ITM call, but the two long calls provide protection, making it less risky than a naked short call.

Q12. Can the Call Backspread be used with index or ETF options?

Yes. It works the same way with stock, ETF, index, or futures options, as long as the ratio is maintained.

Q13. Can the strategy be initiated for a credit?

Sometimes yes, depending on volatility skew. Entering for a credit slightly reduces risk and improves breakeven levels.

Q14. How does it compare to buying a single long call?

A long call has unlimited profit but requires higher upfront cost. A backspread can be cheaper or even free, but carries the risk of a defined loss if the stock stagnates.

Q15. How does it compare to a bull call spread?

A bull call spread has limited risk and limited profit. The backspread has limited risk but unlimited upside, making it more attractive in high-move scenarios.

Q16. Can you create a Put Backspread instead?

Yes. A put backspread is the bearish equivalent: sell one ITM put and buy two OTM puts, betting on a sharp downside move.

Q17. What are the risks of trading this strategy?

- Loss if the stock expires near the long strike.

- Negative Theta (time decay).

- Requires precise timing of the expected move.

Q18. Is the Call Backspread suitable for beginners?

It’s more of an intermediate strategy, since it involves multiple legs and understanding of Greeks. Beginners may struggle with adjustments.

Q19. How do professional traders use Call Backspreads?

They use them during low-volatility conditions as cheap lottery tickets for earnings or events where volatility and price movement are expected to explode.

Q20. Can the Call Backspread be adjusted after initiation?

Yes. Traders may:

- Close part of the long calls to lock profits.

- Roll strikes or expiration.

- Convert into a butterfly or other structure to manage risk.

To keep in mind

The call backspread (reverse call ratio spread) is a versatile bullish options strategy combining the best of both worlds: unlimited upside potential with limited, known risk. By selling ITM calls and buying more OTM calls, traders can create a cost-efficient position that thrives on volatility and strong rallies.

While it is not suitable for every market condition, the call backspread shines in contexts where a sharp breakout is expected. For traders who want to balance risk control with explosive profit potential, this strategy remains a cornerstone of advanced options trading.