- Collar Option Strategy Essentials

- Strategy Essentials

- Introduction to the Collar Strategy

- Construction of the Collar option strategy

- Leverage

- Payoff (Concept)

- Profit Potential

- Loss Potential

- Breakeven

- The Collar Strategy and Option Greeks

- Collar Option Strategy – Example Trade

- Collar Option Strategy Payoff diagram

- Pros & Cons

- FAQ

- To Keep in Mind

Collar Option Strategy Essentials

Strategy Essentials

Construction: Long 100 shares + Sell 1 OTM Call + Buy 1 OTM Put

Maximum Profit: Limited (capped at the short call strike)

Maximum Loss: Limited (protected by the long put)

Breakeven Point: Stock purchase price ± net premium cost

Best Market Context: When holding shares and seeking downside protection while generating income from covered calls

Complexity Level: Beginner to intermediate

Introduction to the Collar Strategy

The Collar option Strategy is a risk-management options strategy widely used by conservative investors. It combines:

- Ownership of the underlying stock (long shares).

- A protective put (insurance against downside).

- A covered call (to generate premium income).

In simple terms, a collar places a “floor” below the stock price (thanks to the put) and a “cap” above (because of the short call).

This strategy is particularly attractive for long-term investors who:

- Want to protect profits in a stock that has recently appreciated.

- Want to limit downside risk without selling their shares.

- Don’t mind capping their upside in exchange for peace of mind.

Construction of the Collar option strategy

The classic construction looks like this:

- Buy 100 shares (assuming that the option contract size is 100) of the stock (or already own them).

- Sell 1 out-of-the-money call option against those shares (covered call).

- Buy 1 out-of-the-money put option (protective insurance).

Both the put and call should have the same expiration month and the same number of contracts.

Key Idea:

- The short call generates premium to offset the cost of the protective put.

- The long put sets a safety floor in case the stock collapses.

This is why the collar option strategy is often described as a hedged covered call.

Leverage

A collar option strategy is not a leveraged strategy in the traditional sense, because you must own the underlying shares.

- Minimum requirement: 100 shares of the stock per collar.

- Buying the shares ties up capital, so returns are more modest compared to naked options plays.

- However, the risk-adjusted return is superior because losses are capped.

For traders managing larger portfolios, collars can be scaled across multiple lots of 100 shares.

Payoff (Concept)

The payoff of a collar resembles a range:

- Upside is capped at the short call strike.

- Downside is limited at the protective put strike.

- Between these levels, the stock fluctuates and profits/losses vary, but the collar ensures no catastrophic loss.

Graphically, it looks like a flat floor and a flat ceiling with a slope in between.

Profit Potential

In a collar option strategy, profit is capped because of the short call.

Formula:

Max Profit = Short Call Strike – Purchase Price of Stock + Net Premium Received – CommissionsProfit occurs when:

The stock closes at or above the short call strike at expiration.

This makes the collar less appealing in runaway bull markets, since you must give up gains above the call strike.

Loss Potential

In a collar option strategy, loss is limited by the long put.

Formula:

Max Loss = Purchase Price of Stock – Long Put Strike – Net Premium Received + CommissionsLoss occurs when:

The stock crashes below the long put strike.

This feature makes collars very popular among conservative investors who prefer defined outcomes.

Breakeven

The breakeven for a collar option strategy depends on the net premium cost (or credit).

Formula:

Breakeven = Purchase Price of Stock ± Net Premium (Debit/Credit)- If the collar is entered at net zero cost, breakeven ≈ stock purchase price.

- If the put is more expensive than the call, breakeven rises slightly.

- If the call premium exceeds the put cost, breakeven falls.

The Collar Strategy and Option Greeks

The Collar Strategy is not only defined by its payoff profile, but also by the way it behaves with respect to the option Greeks. Understanding how Delta, Gamma, Theta, Vega, and Rho interact in a collar is essential to fully grasp the dynamics of this protective options strategy.

Delta – Directional Exposure

- A collar is constructed with long stock (Delta ≈ +1), long put (Delta negative), and short call (Delta negative).

- The combined Delta is positive but reduced, meaning the position is still bullish, but with muted upside potential.

- Example:

- 100 shares = +100 Delta

- Long OTM put = –30 Delta

- Short OTM call = –25 Delta

- Net Delta ≈ +45 → you still profit if the stock rises, but much less than with stock alone.

The Collar reduces overall directional exposure, protecting against sharp drops while limiting gains if the stock rallies.

Gamma – Sensitivity to Stock Movements

- The Collar has low Gamma.

- Since both the protective put and the short call are OTM options, their Gamma is modest until the stock approaches the strikes.

- Near the call strike, the short call’s Gamma rises, capping gains quickly. Near the put strike, the put’s Gamma increases, enhancing downside protection.

The Collar is a low-Gamma, low-volatility profile compared to naked stock.

Theta – Time Decay

- Theta is usually close to neutral in a Collar.

- The short call generates positive Theta (earning premium as time passes).

- The long put generates negative Theta (losing value with time).

- The stock has no Theta component.

- Net effect → Theta often cancels out or results in a small positive value if the call premium is larger than the put’s cost.

- Many traders like collars because they are not heavily penalized by time decay.

Vega – Sensitivity to Volatility

- The Collar is short Vega, because:

- Long put = Vega positive

- Short call = Vega negative

- Their Vega exposures offset each other.

- In practice, the Collar’s Vega exposure is close to neutral.

- Rising volatility slightly helps the protective put, but it also increases the liability of the short call.

This makes the Collar a volatility-insensitive strategy, compared to pure long puts or straddles.

Rho – Sensitivity to Interest Rates

- Long puts have negative Rho.

- Short calls have positive Rho.

- With stock in the mix, the overall Rho impact is minor.

- Net effect → Collars are largely insensitive to interest rate changes.

| Greek | Effect in Collar | Interpretation |

|---|---|---|

| Delta | Moderately positive | Bullish bias, capped by short call |

| Gamma | Low | Smooth reaction, limited convexity |

| Theta | Near neutral | Time decay mostly balanced |

| Vega | Near neutral | Limited sensitivity to volatility shifts |

| Rho | Minimal | Rates have little impact |

Note

- The Collar strategy reduces Delta exposure, making it safer than owning stock outright.

- It balances Theta and Vega, keeping the position resilient to time decay and volatility.

- It provides defined risk and defined reward, making it a favorite among conservative investors.

- Traders must understand that while the Collar protects against large losses, it also forfeits large gains due to the short call

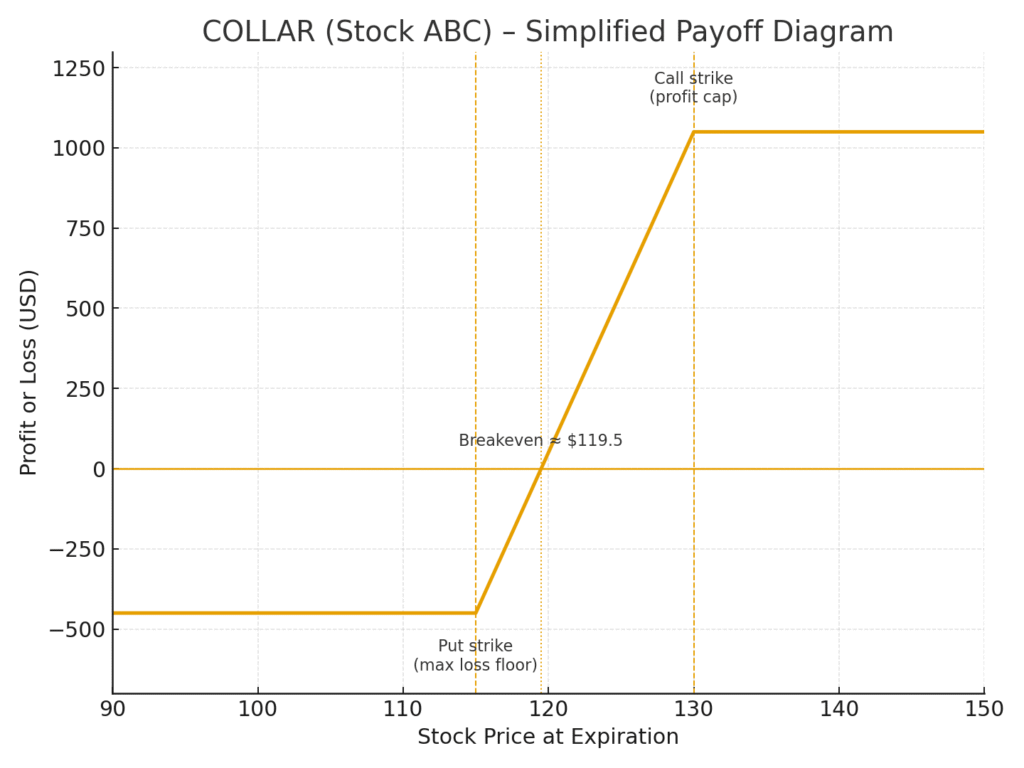

Collar Option Strategy – Example Trade

Let’s build a real-world style example.

- Stock ABC trades at $120.

- Trader buys 100 shares at $120 = $12,000.

- Sells 1 February 130 Call for $3.00 = $300 premium.

- Buys 1 February 115 Put for $2.50 = $250 cost.

Net Premium = +$50 credit.

Total effective investment = $11,950.

Scenarios at Expiration

1️⃣ Stock at $140 (well above short call strike):

- Shares called away at $130 → receive $13,000.

- Net result = $13,000 – $11,950 = $1,050 profit (max profit).

2️⃣ Stock at $120 (unchanged):

- Call expires worthless.

- Put expires worthless.

- Value = $12,000 – $11,950 = $50 profit (thanks to net credit).

3️⃣ Stock at $110 (big drop):

- Call worthless.

- Put kicks in at 115 → sell shares for $11,500.

- Net = $11,500 – $11,950 = $450 loss (max loss).

➡️ Summary:

- Max Profit = $1,050 (capped).

- Max Loss = $450 (limited).

- Breakeven = $119.50 (purchase 120 – net credit 0.50).

Collar Option Strategy Payoff diagram

Pros & Cons

Advantages:

- Protects downside risk.

- Generates income via call premium.

- Defined risk/reward profile.

- Simple to manage for stockholders.

Disadvantages:

- Requires owning shares (capital intensive).

- Profit potential is capped.

- May underperform if the stock skyrockets.

- Less effective in very low volatility markets (options premiums too cheap).

FAQ

Q1. What is a Collar Strategy in options trading?

A Collar Strategy is an options hedge that combines owning shares of stock with the purchase of a protective put and the sale of a covered call. It is used to limit downside losses while also capping upside gains.

Q2. Why do traders use the Collar Strategy?

Investors use collars to protect profits, hedge downside risk, and stabilize portfolio returns. It’s especially useful for investors who want insurance against a market downturn without selling their shares.

Q3. Is the Collar Strategy bullish or bearish?

It’s generally moderately bullish. The strategy works best if the stock rises modestly, but it’s mainly defensive in nature.

Q4. How is a Collar constructed?

- Long 100 shares of stock

- Buy 1 out-of-the-money put (downside protection)

- Sell 1 out-of-the-money call (income to offset the put cost)

Q5. What is the maximum profit of a Collar ?

The maximum profit is limited to the difference between the short call strike and the stock purchase price, adjusted for net premiums.

Q6. What is the maximum loss of a Collar?

The maximum loss is limited and occurs if the stock crashes below the protective put strike. Loss = Purchase price – Put strike ± net premium.

Q7. What is the breakeven point of a Collar?

Breakeven depends on whether the collar was opened for a debit or credit:

- Debit → Purchase price + net cost

- Credit → Purchase price – net credit

Q8. What is a costless collar?

A “costless” or “zero-cost collar” happens when the premium received from the short call equals or exceeds the cost of the protective put.

Q9. When is the Collar Strategy most effective?

When implied volatility is relatively high (puts are valuable) and when the investor wants to lock in profits without selling stock.

Q10. Can I use the Collar Strategy with ETFs or indexes?

Yes. Collars can be applied to ETFs, index options, and even futures options, not just individual stocks.

Q11. Does the Collar Strategy require a large investment?

Yes, because you need to own at least 100 shares of the stock for each collar. This makes it more capital-intensive compared to pure options strategies.

Q12. How does volatility affect a Collar?

Higher volatility makes puts more expensive, which can increase collar costs. However, it also increases the premiums collected from selling calls.

Q13. Can I adjust a Collar after opening it?

Yes. Traders can roll the short call up or out, close the put early, or adjust strikes to lock in more profit or lower costs.

Q14. How do commissions affect the Collar Strategy?

Commissions slightly reduce net profit and protection. For frequent traders, choosing a low-cost broker is important.

Q15. Is the Collar Strategy suitable for beginners?

Yes. It’s considered one of the safest option strategies since both profit and loss are defined at entry.

Q16. How does a Collar compare to a Covered Call?

A covered call has no downside protection. A collar is essentially a covered call with an added protective put.

Q17. How does a Collar compare to a Protective Put?

A protective put offers full downside insurance but costs money. A collar offsets part (or all) of this cost by selling a call.

Q18. What happens if the stock price soars above the short call strike?

The shares are called away at the strike price. You keep the profit up to that strike but miss any gains beyond.

Q19. What happens if the stock collapses below the long put strike?

You exercise the put, selling the shares at the put strike, limiting losses. The short call expires worthless.

Q20. Can a Collar be used in retirement accounts?

Yes. Since it is a defined-risk strategy and involves no naked options, collars are generally allowed in IRAs and other retirement accounts (depending on the broker).

To Keep in Mind

- Collars are not designed for speculation but for capital protection.

- They work best when you already own stock and want insurance.

- A “costless collar” is ideal but not always possible.

- Always account for commissions and spreads, as they impact net outcomes.

The Collar Strategy is one of the safest and most popular defensive option strategies. It limits losses through a protective put while generating income through a covered call, at the expense of capped profit potential.

For investors who want to sleep well at night while holding volatile stocks, the collar provides peace of mind by defining both the maximum loss and maximum gain in advance.