To answer the question how do interest rates affect option prices, first, let’s take a closer look at the extrinsic components of option pricing : volatility (Vega), time to maturity (Theta), dividends and Interest rates with Rho being one of them.

The theoretical price of an option is based on the Black-Scholes model.

One of the inputs in this formula is the one-year U.S. Treasury yield, which serves as the so-called risk-free rate.

This “risk-free rate” =>r is a cornerstone of finance:

- It represents the return investors can earn without taking on any risk (by holding deposits or government bonds).

- It also sets the benchmark for borrowing costs across the economy.

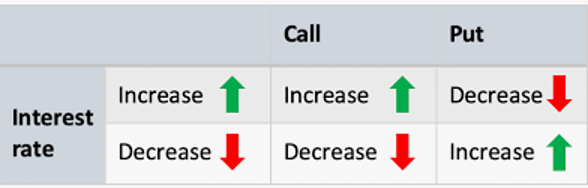

When the risk-free rate rises, market participants are generally less inclined to take risks on equities or alternative investments with higher volatility. Conversely, when rates fall, risk assets tend to attract more capital.

The Basic Rule of Thumb

- Rising rates = falling stock markets

- Higher borrowing costs: companies finance at higher rates, which reduces investments and future profits.

- Bonds and fixed-income products become more attractive relative to equities, leading to capital outflows from stock markets.

- Household consumption slows because loans are more expensive, which indirectly reduces company revenues.

- Falling rates = rising stock markets

- Lower borrowing costs: companies can borrow at cheaper rates, encouraging investment and growth.

- Bonds yield less, making equities relatively more attractive, which redirects capital flows toward stocks.

- Household spending accelerates with cheaper credit, boosting corporate earnings.

In other words, central banks use interest rate adjustments as a lever to cool down the economy in times of inflationor to stimulate growth during recessions.

But What About Options?

To understand the correlation between option pricing and interest rates, consider a comparison:

- Trader A buys the underlying directly (e.g., a stock).

- Trader B uses options (calls or puts) on that same underlying.

Both traders either borrow money to take long positions (stock purchase vs. call/put buying) or receive interest when shorting (short stock vs. short calls/puts).

Rho – The Interest Rate Greek

Among the Greeks, the metric that captures the impact of interest rate changes is Rho (ρ).

Rho measures how the premium of an option changes when interest rates move by 1%.

- For a Call option: Rho is positive.

- For a Put option: Rho is negative.

Example

- Call Option: Premium = $10, Rho = +0.3.→ If the 1-Year Treasury rate rises by 1%, the call premium increases to $10.30.

- Put Option: Premium = $10, Rho = –0.3.→ If the 1-Year Treasury rate rises by 1%, the put premium decreases to $9.70.

Summary:

| Long Call | Long Put | Short Call | Short Put | |

| Rho | + | – | – | + |

Impact of Rate Changes on Option Premiums

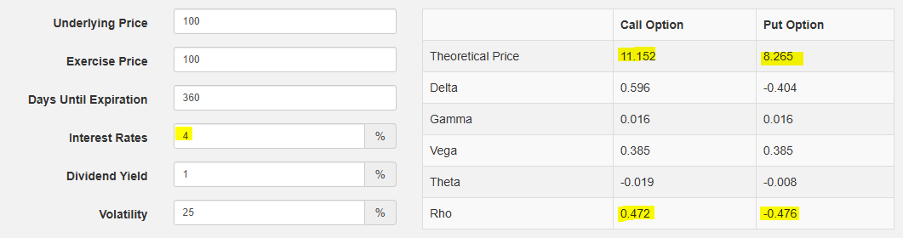

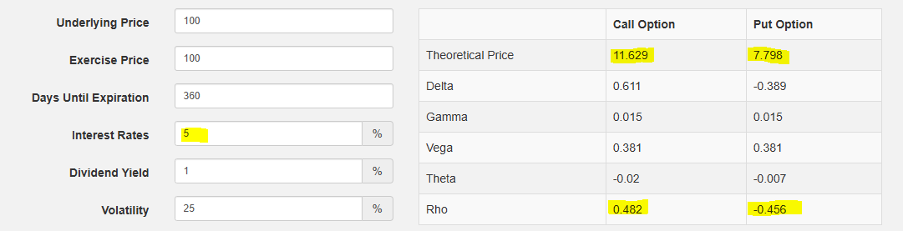

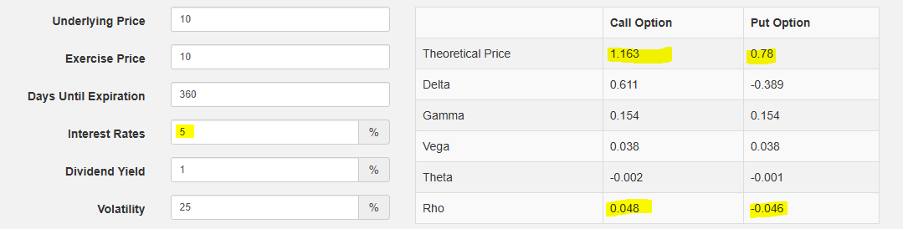

Let’s take an at-the-money option with an underlying at $100, strike at $100, and long-term maturity of 1 year (360 days to expiration). We hold dividends and volatility constant.

- With an interest rate of 4%:

- Call Price = $11.152

- Put Price = $8.625

With an interest rate of 5% (+100 basis points):

- Call Price = $11.629

- Put Price = $7.798

Observations:

- The call premium increases by $0.477 (from 11.152 → 11.629): positive rho increasing 0,01

- The put premium decreases by $0.827 (from 8.625 → 7.798); negative rho increasing 0,02

As expected, a 1% rate hike raises call premiums and reduces put premiums, almost symmetrically in absolute value — reflecting the effect of Rho.

Frequency of Rate Changes

Interest rate adjustments are determined by the Federal Reserve (Fed).

- They usually occur no more than 3–4 times per year (except in extraordinary circumstances like recessions or overheating economies).

- Adjustments are often modest, typically 25 to 50 basis points.

Moreover, while interest rate changes do affect option premiums, their impact is often overshadowed by the much larger effect on the underlying assets (stocks, indices, commodities). A rally in equities can completely outweigh the small premium variation induced by Rho.

The Bigger Picture

We have demonstrated that although interest rates (through Rho) do influence option pricing, their effect is generally modest compared to other variables such as volatility or the price of the underlying.

However:

- The longer the maturity of the option, the greater the impact of Rho. This is particularly true for LEAPS (Long-Term Equity Anticipation Securities), where sensitivity to interest rates compounds over time.

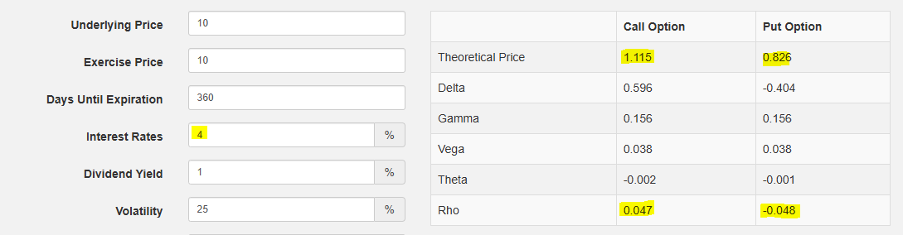

- Rho values also vary with the price level of the underlying. For example, Rho increases significantly as the underlying’s price rises. In some cases, a tenfold increase in the underlying price can lead to a tenfold increase in Rho.

Conclusion

Rho is an important but often overlooked Greek.

- Yes, interest rates impact option premiums.

- But the effect is usually secondary compared to volatility and the price of the underlying.

- Traders should be mindful of Rho primarily for long-dated options (LEAPS) and for underlyings with higher notional values.

FAQ

Q1: What is Rho in options trading?

Rho is one of the “Greeks,” a sensitivity measure that shows how much the price of an option will change when interest rates move by 1%. A positive Rho means the option’s premium increases with higher rates (typical for calls), while a negative Rho means the premium decreases (typical for puts).

Q2: Why are interest rates considered in the Black-Scholes model?

The Black-Scholes model requires the risk-free rate as an input because it reflects the theoretical return of holding cash or risk-free bonds. It affects the present value of expected payoffs from options. Without this, the model would ignore a major component of financial markets: the time value of money.

Q3: Do interest rates have a large impact on option prices?

Generally, no. While rates do matter, their effect is typically modest compared to other variables such as the underlying asset’s price, volatility, and time to expiration. Rho becomes more important for long-dated options and high-priced underlyings.

Q4: Why is Rho positive for calls and negative for puts?

- For calls, higher rates make it relatively cheaper to hold calls instead of buying the underlying stock with borrowed funds, so call premiums rise.

- For puts, higher rates reduce their attractiveness, since shorting the underlying yields interest; thus, put premiums fall.

Q5: How often does the Fed change interest rates?

Normally 3–4 times per year, unless there is an economic shock (like a recession or inflation surge). Changes are often in increments of 25 to 50 basis points (0.25–0.50%), though extreme situations may call for larger moves.

Q6: Are Rho effects more significant for LEAPS?

Yes. LEAPS (Long-Term Equity Anticipation Securities) have maturities of up to two years or more. The longer the time horizon, the more sensitive the option premium becomes to interest rate changes, making Rho an important factor.

Q7: How does volatility interact with interest rates in option pricing?

Volatility often overshadows Rho. For instance, a 1% change in interest rates may alter a premium by a few cents, while a surge in implied volatility can change it by several dollars. That’s why most traders prioritize Vega over Rho in day-to-day trading.

Q8: What happens to Rho if the underlying stock price increases?

Rho generally increases as the underlying’s price rises. For example, moving from a $10 stock to a $100 stock can multiply Rho values by ten. This is because the option’s notional exposure grows with the underlying’s price.

Q9: Do dividend-paying stocks affect Rho?

Yes. Dividends interact with interest rates in pricing models. Higher dividend yields can reduce call prices and increase put prices, partially offsetting Rho effects. That’s why traders analyze both Rho and dividend yield when pricing options on dividend-paying stocks.

Q10: How do interest rates affect spreads like bull call spreads or bull put spreads?

For spreads, the net Rho is the difference between the Rho values of the two legs. In many cases, the impact cancels out partially. This means that for vertical spreads, the sensitivity to interest rates is usually lower than for outright long calls or puts.

Q11: Is Rho more important for institutional traders than retail traders?

Yes. Hedge funds, pension funds, and other institutions often trade long-dated, high-notional options where interest rate sensitivity can have a meaningful impact. For retail traders dealing in short-term options, Rho is usually less significant.

Q12: Does Rho matter more in high-interest-rate environments?

Absolutely. When rates are near zero, Rho’s influence is almost negligible. But in a high-rate environment (e.g., Fed funds above 5%), Rho can have a larger absolute effect on option pricing.

Q13: How should traders incorporate Rho in their strategy?

- Short-term retail traders → focus mainly on Delta, Vega, and Theta.

- Long-term or institutional traders → monitor Rho closely, especially on LEAPS, indexes, and interest-rate sensitive underlyings.

Q14: Can changes in Rho create arbitrage opportunities?

Not directly. Rho is a model sensitivity, not a tradable variable. However, if options are mispriced because of overlooked rate changes, arbitrageurs may step in using interest-rate parity relationships to realign prices.

Q15: Why is Rho often ignored by beginners?

Because for most short-term, low-notional trades, the effect of Rho is tiny. For example, a 0,25% rate move might change a $5 option premium by only a few cents. Beginners naturally focus more on Delta, Theta, and Vega, which dominate short-term price movements.

Key Takeaways

- Interest rate variations directly influence option pricing.

- In the Black-Scholes model, the input is the risk-free rate (1-Year U.S. Treasury, set by the Fed).

- When rates rise → call premiums increase while put premiums decrease.

- Rho is the Greek that quantifies this effect.

- The impact is more significant on longer maturities and higher-priced underlyings.

{kind=link}